John Stepek says the price of gold is a gauge of investment fear — and there’s a lot of fear around right now

Last week, we had a power cut. It was already pitch-dark outside — not the best time to discover that the children had hidden our only torch. We stumbled about in the dark, before a kindly neighbour gave us some candles and a lighter — just as the power went back on.

It was a useful reminder that you can rely on the modern world to function about 99 per cent of the time, but it’s always worth having an old-fashioned back-up, just in case. When the National Grid cuts out, you want candles in your drawer. When the global financial system starts to wobble, you want good old-fashioned gold in your portfolio.

But why? Gold makes no sense as an investment. The point of most investment assets is that they generate income. The price that a sensible investor is willing to pay for an asset should reflect the amount of future income it is expected to provide. An investment property is supposed to pay the owner a rent — though not always, as many city-centre buy-to-let amateurs are finding to their cost. You buy shares in a company either because it pays a dividend or because you expect it to reach a position where it pays a dividend in the future. Even current accounts (effectively a loan to the bank, as Northern Rock account-holders have learnt rather vividly in recent weeks) pay some minimal level of interest.

Gold doesn’t pay anything. In fact, gold costs the owner money, in the form of charges for storage and insurance. The only possible way to make money from gold is if you can sell it for more than you bought it for.

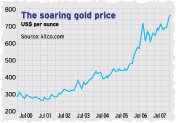

However, this misses the point. Gold is better seen as an insurance than as an investment. Gold tends to become more popular when investors are worried about the possibility of a financial crisis. Think of the gold price as a gauge of investment fear — and with an ounce of gold currently selling at a 28-year high of more than $740, there’s a lot of fear around.

Northern Rock was just a very obvious symptom of a much deeper problem currently facing the global financial system. Massive bad debts, which have been built up by banks lending carelessly to the sub-prime end of the US housing market, have been spread far and wide across the world through the use of credit derivatives. With no one really sure of where these losses are going to spring up next, banks have suddenly become much more picky about who they lend to. But the property bubbles currently afflicting most Western countries have been built on easy lending. Soaring house prices have also fuelled a consumer boom on both sides of the Atlantic, leaving much of the population reliant on credit lines which are now rapidly going to be taken away from them.

The obvious solution — though not necessarily the correct one — is for central banks to lower interest rates and try to pump the system full of money again. Indeed, the US Federal Reserve has already slashed dollar interest rates by half a percentage point. The trouble is, this makes the dollar look even less attractive to the foreign investors who have been propping up the American economy for so long. But as analysts John Hill and Graham Wark of Citigroup asked in a recent research note, what’s the alternative to the dollar, currently the world’s reserve currency? Most countries blah blah on the US consumer being able to buy their exports. So no other country actually wants a strong currency. And if you can’t put your faith in any paper-based currency, then what can you trust? This is where gold comes in. Gold has been used as a reliable store of wealth for millennia – in fact, our currency system still had some form of gold-backing right up until 1971. If there was a nuclear war tomorrow, the survivors would be dollar bills and pound notes as fire-lighters. But as a durable, desirable physical asset, gold would still retain some purchasing power.

Even if yu don’t buy the financial Armageddon scenario yourself, you can profit from the fact that others do There’s not that much gold to go round. Demand is rising as investors in increasingly wealthy emerging market countries, India in particular, buy more. Supply is constrained by the soaring costs of developing new mines. As top-performing fund manager Nils Taube recently told the Daily Telegraph’s Tom Stevenson ‘it doesn‘t need many to think gold’s important for there to be an explosion in the price.’ As Taube points out, gold was a ‘great performer’ in 1987 and 1974, both times of financial panic.

You can buy physical gold in the form of bars or sovereign and krugerrand coins from bullion dealers such as Chards (www.chards.co.uk) and Bairds (www.goldline.co.uk). But as you can imagine, secreting a stash of gold coins in your home has implications for security and insurance, while storing them somewhere else will result in storage charges.

A more convenient way to profit from the rising attractiveness of gold is to buy into one of the several London Stock Exchange-listed funds that track the gold price. The good news is that you can even pop one of these funds – the ETF Securities Physical Gold fund, London-listed under the ticker code PHAU – in your tax-efficient Isa account, thus protecting any capital gains from the Inland Revenue‘s clutches. For more information, see www.etfsecurities.com.

And don’t worry about the fact that gold is priced in dollars. The US currency is weak, and likely to get weaker, but as the dollar weakens, gold tends to strengthen proportionately, so any fall in the dollar is offset. Secondly, as the chart shows, while gold has advanced 130 per cent in the last five years against the dollar, it‘s also managed a more-than-respectable 76 per cent against the pound over the same period.

Lastly, our own currency hasn‘t got much going for it either. It may not yet be as sickly as the dollar, but once house prices start to fall nationwide and with the future of interest rates less certain, sterling might just stop looking so attractive to foreign traders. HSBC reckons the pound could fall to as low as $1.76 within the next 18 months. That of course, would be good news for anyone who bought gold now, while a pound still fetches more than two US dollars.

John Stepek is deputy editor of MoneyWeek.

Comments