People respond to incentives. And in market economies, few incentives top profits. In the energy industry, oil prices are a crucial determinant of drillers’ profits — and therefore, their behaviour. When a supply glut crushed Brent crude oil prices by -77 per cent from June 2014 to January 2016, drillers focused on areas where they could reduce costs, shuttering rigs they couldn’t run profitably.[i] Yet now, with prices snapping back 194 per cent from their low, incentives have changed.[ii] And, accordingly, oil drillers are deploying assets globally, putting rigs back to work and expanding activity. Seeing that, you may wonder if UK production is due for an upturn, boosting the British economy with it. But in our view, it is unlikely oil’s upturn will have a marked effect on UK production absent much higher prices, which we don’t expect.

During oil’s two-year downturn, production and activity were hard hit globally. According to oil services firm Baker Hughes, an average 3,578 rigs were active per month drilling for oil and gas globally in 2014.[iii] In 2016, after oil’s collapse, this was down to an average 1,593 rigs — that is how drastically drillers curtailed activity. But now, with prices up, activity is rebounding. An average 2,162 rigs have been active each month this year to date.

Yet despite the upswing, UK drilling activity is lagging. In May, for example, Baker Hughes’s tally showed only five rigs active in UK waters.[iv] Unlike most of the world, this is down from a year ago, when ten rigs drilled for oil and gas off the UK’s shores.

It seems as though activity is perking a bit lately, though. In late May, the UK Oil and Gas Authority (OGA) published the results of its latest licensing rights auction. These bids, in which oil firms aim to acquire exclusive rights to search for oil in a designated section of the UK continental shelf from the government, have garnered little interest in recent years, tied to low oil prices. But in May, OGA announced it sold 123 licenses.[v] The OGA called this ‘transformational’. OGA Chief Dr Andy Samuel said: ‘The UKCS [continental shelf] is back. Big questions facing the basin have been answered in this round. Exploration is very much alive with lots of prospects generated and new wells to be drilled.’

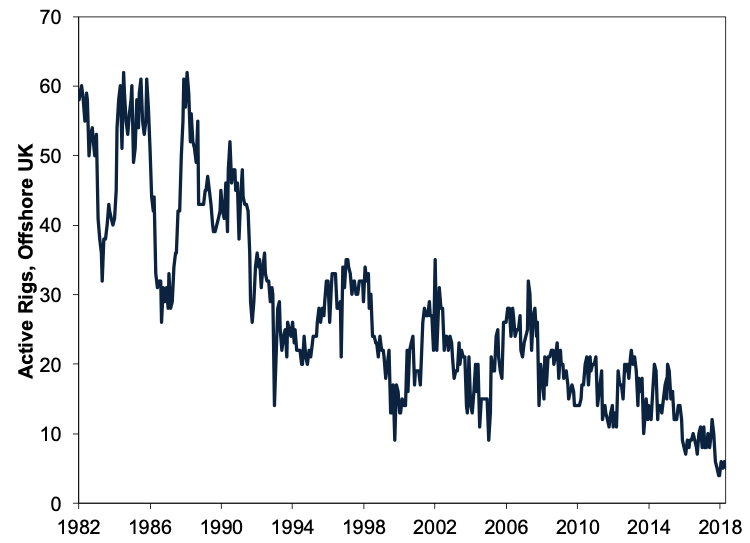

Sounds rosy. But we doubt the staying power. Many UK North Sea oil fields, in operation for decades, are nearing the end of their operational lifespans. This is why UK rig activity has been trending down for the past three decades. (Exhibit 1)

Exhibit 1: UK offshore rig count

Source: GE Baker Hughes International Rig Count, January 1982 – May 2018 (full data series).

Another reason North Sea production has been under pressure in recent years: costs. It is more expensive to drill in this region than in the fast-growing US shale oil fields, particularly after cost cuts shale drillers made in recent years. For example, Shell Oil estimates that, once it is producing, the North Sea project it began in January will require Brent crude prices of $40/barrel to cover expenses. Oil crossed that mark initially in late 2016, but in the present post-oil-crash environment, many firms have been cautious about investing until there is a price cushion. By contrast, in the American state of Texas’s Permian Basin — the world’s most productive oil field — shale firms can cover costs on existing wells at an average $25 per barrel. That it is likely why drilling activity in Texas is up from a 20 May 2016 low of 173 rigs to 536 on 8 June this year.[vi]

Now, the UK has its own shale oil fields (primarily, the Bowland Shale), and firms could employ the same techniques there that they have used to such great effect in America. Actually, on a very small scale, they already are. In April, privately owned Cuadrilla Resources drilled the UK’s first horizontal well — a key technique pioneered on US shale fields. Perhaps, if this practice grows, UK output can follow the US model. But there are headwinds.

Key to America’s shale oil production revolution, in our view, is the fact landowners own mineral rights for the oil under their property. Hence, oil firms pay them royalties or fees — they have an economic interest in allowing drilling on their land. In the UK, the Crown owns mineral rights. Perhaps as a result, land drilling in the UK has never been very common. After all, who wants to see land in their community — or on their property — scarred by drilling if there is nothing in it for them? This complicates overcoming virulent political opposition to onshore oil drilling.

If oil prices rise sufficiently, firms will likely try to find a way to overcome these obstacles. Yet those higher prices aren’t likely in the near future, in our view. US oil output hit a record 10.47 million bpd in March and the US Energy Information Administration’s weekly estimates put it at 10.8 million in May.[vii] This is a key reason why the International Energy Agency projected oil supply growth outstripping demand growth this year, which should weigh on prices.[viii] But also, Saudi Arabia reportedly increased output in May, and Russia reportedly wants to loosen the cap it agreed to with OPEC. This all points to rising production and relatively stable prices. If that happens, we believe it is unlikely UK production surges — either in relatively costly North Sea fields or from newer onshore sources struggling to launch.

Fisher Investments Europe Limited, trading as Fisher Investments UK, is authorised and regulated by the UK Financial Conduct Authority (FCA Number 191609) and is registered in England (Company Number 3850593). Fisher Investments Europe Limited has its registered office at: 2nd Floor, 6-10 Whitfield Street, London, W1T 2RE, United Kingdom.

Investment management services are provided by Fisher Investments UK’s parent company, Fisher Asset Management, LLC, trading as Fisher Investments, which is established in the US and regulated by the US Securities and Exchange Commission. Investing in equity markets involves the risk of loss and there is no guarantee that all or any invested capital will be repaid. Past performance neither guarantees nor reliably indicates future performance. The value of investments and the income from them will fluctuate with world equity markets and international currency exchange rates.

Follow the latest market news and updates from Fisher Investments UK:

[i] Source: FactSet, as of 11/6/2018. Brent crude oil price, 23/6/2014 – 20/1/2016.

[ii] Ibid. Brent crude oil price, 20/1/2016 – 31/5/2018.

[iii] Source: GE Baker Hughes, as of 12/6/2018. Worldwide Rig Count, May 2018.

[iv] Ibid. International Rig Count, May 2018. Number of rigs active UK territorial waters.

[v] Source: UK Oil & Gas Authority, as of 12/6/2018.

[vi] Source: GE Baker Hughes, as of 12/6/2018. State of Texas onshore rig count.

[vii] Source: US Energy Information Administration, as of 12/6/2018. US Monthly Crude Oil Production as of March 2018 and Weekly Supply Estimate, as of 1/6/2018.

[viii] Source: International Energy Agency, as of 12/6/2018. Oil Market Report for May 2018.

Fisher Investments Europe Limited, trading as Fisher Investments UK, is authorised and regulated by the UK Financial Conduct Authority (FCA Number 191609) and is registered in England (Company Number 3850593). Fisher Investments Europe Limited has its registered office at: 2nd Floor, 6-10 Whitfield Street, London, W1T 2RE, United Kingdom.

Investment management services are provided by Fisher Investments UK’s parent company, Fisher Asset Management, LLC, trading as Fisher Investments, which is established in the US and regulated by the US Securities and Exchange Commission. Investing in equity markets involves the risk of loss and there is no guarantee that all or any invested capital will be repaid. Past performance neither guarantees nor reliably indicates future performance. The value of investments and the income from them will fluctuate with world equity markets and international currency exchange rates.

This document constitutes the general views of Fisher Investments UK and Fisher Investments, and should not be regarded as personalised investment or tax advice or as a representation of their performance or that of their clients. No assurances are made that they will continue to hold these views, which may change at any time based on new information, analysis or reconsideration. In addition, no assurances are made regarding the accuracy of any forecast made herein. Not all past forecasts have been, nor future forecasts may be, as accurate as any contained herein.

For more information, visit fisherinvestments.com/en-gb.

Comments