“Equities seem so uncertain now. I’ll just wait until the market settles down—then I’ll make a move.”

Many investors may think this statement makes sense at first—waiting until market volatility settles, or a correction or bear market recovers before putting your money into equities.

But what exactly is the sign investors are waiting for? If you’re waiting for a clear sign that volatility in equities has subsided and will start appreciating in neat, steady steps, you may end up waiting forever. Equities are volatile by nature, and even their volatility can be volatile. It’s the volatility and risk that enables equity returns to grow the way they historically have. To get lower shorter-term volatility, you’d have to expect lower longer-term returns. Waiting for volatility to stop could mean waiting a very long time!

Some of equities’ most volatile days can occur during the steep, bottom period of a bear market or correction. It may seem that a smart move is waiting until the bear market is over and the new bull is under way before putting more money in the market. If you’re currently invested you may wonder: Should you exit the market and then get back in when the volatility clears up? How do you choose the right time to jump back in?

No one can perfectly time markets. Sure, you might get lucky! But you can’t count on luck as a strategy. As painful as late bear market wild wiggles are in the shorter term, you don’t want to miss the start of a new bull market. New bull market returns are quick and massive—they can quickly erase almost all late-stage downside volatility.

A typical bear market works like a spring. The more you depress it, the bigger the bounce. It is possible for a bear markets to double-bottom, but that doesn’t lessen the effect of the bounce up. And given enough time, those W-shaped bottoms can resolve into more of a V-shape.

Deteriorating fundamentals drive the initial drop of a bear market. Folks think bear markets start with a bang—they usually don’t. Corrections start like that—a big, sentiment-driven drop that scares the pants off almost everyone. It would be much easier if bear markets had that big, scary announcement factor. “Hey! Big bear coming!” But the reality is bull market tops tend to roll over, and the new bear slowly grinds lower.

A rolling bull market top can be misleading. If there was a huge, all-of-a-sudden indicator, investors could see a bear coming and get out with minimal damage—but that’s not usually the case. It’s actually later in the bear market when a sudden “bang” occurs. Sentiment and a decrease in liquidity take over from the deteriorating fundamentals, which can lead to panic.

However, it’s usually the lack of liquidity and sentiment movement that is causing the panic—not something fundamental. Equity valuations often become detached from reality. Timing bear market bottoms during these panic-driven times is especially tough. It’s difficult to measure how accurately sentiment reflects reality. And sentiment moves fast. Which is why, as a new bull market starts, the right side of the V-shape bottom can happen just as fast.

In the early stages of a bull market, many investors may simply not believe that a bull has begun. This disbelief could last for years, but it’s particularly profound in the beginning. Everything seems so bad.

And everything probably is pretty bad. Equities can start rising before the economy has even fully bottomed. But equities don’t boom because things are improving. It’s the movement in sentiment that helps equities achieve the steep bounce off the bottom. Even a small reduction of negative sentiment combined with hugely depressed valuations can make equities take off like a bullet. And the shape of the initial stage of the new bull market typically about matches the speed and shape of the end of the bear—a “V-bounce” effect.

It’s not just theory—we see the V through history. Exhibits 1 through 4 show some of history’s V-bounces.

Exhibit 1: A Real V-Bounce—1942

Source: Global Financial Data, Inc., as of 31/12/2018, S&P 500 Total Return Index (monthly data) from 30/06/1941 to 31/12/1943. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns. For S&P 500 Price Index performance over the previous 5 years, please reference Exhibit 6.[i]

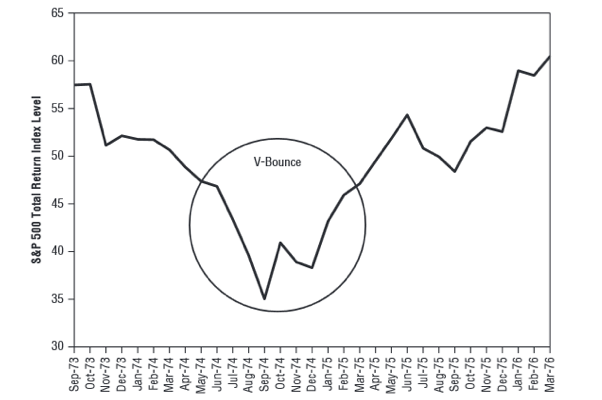

Exhibit 2: A Real V-Bounce—1974

Source: Global Financial Data, Inc., as of 31/12/2018, S&P 500 Total Return Index (monthly data) from 30/09/1973 to 31/03/1976. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns. For S&P 500 Price Index performance over the previous 5 years, please reference Exhibit 6.[ii]

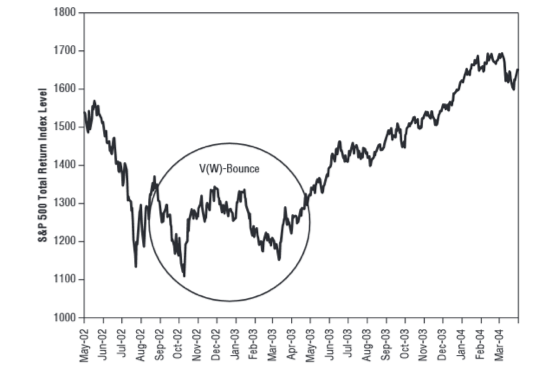

Exhibit 3: A Real V-Bounce—2002

Source: Global Financial Data, Inc., as of 31/12/2018, S&P 500 Total Return Index (monthly data) from 31/05/2002 to 31/03/2004. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns. For S&P 500 Price Index performance over the previous 5 years, please reference Exhibit 6.[iii]

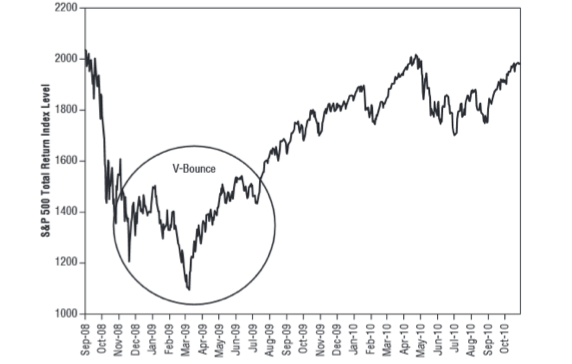

Exhibit 4: A Real V-Bounce—2009

Source: Global Financial Data, Inc., as of 31/12/2018, S&P 500 Total Return Index (monthly data) from 30/09/2008 to 31/10/2010. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns. For S&P 500 Price Index performance over the previous 5 years, please reference Exhibit 6.[iv]

What happens if you wait for “clarity” before getting back in the market? That can mean missing your chance to erase a big portion of your prior bear market losses. The huge V-bounce returns are early. Protecting yourself from potential further negative volatility can feel good at first. But it can rob investors of the huge returns we normally get from the early bull V-bounce that may help put you on the way to recovery.

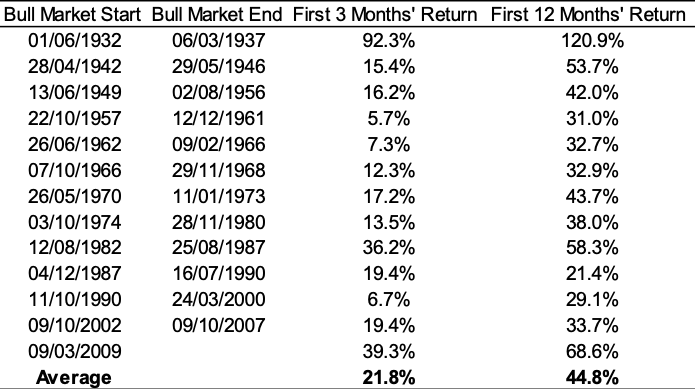

During the time around the bottom of the V-bounce, you may not know which volatility you’re suffering through—late bear or early bull. But if you miss those early returns, you will regret it. Exhibit 5 shows how massive those early returns can be—averaging 21.8 percent in the first 3 months and 44.8 percent in the first 12 months. A bull market’s average annual return is 21 percent[v]—but a bull market’s average first year more than doubles that!

Exhibit 5: First 3 and 12 Months of a New Bull Market—S&P 500

Source: Global Financial Data, Inc., as of 31/12/2018, S&P 500 Price Index average is calculated for all bull market periods ending 09/10/2007. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns. For S&P 500 Price Index performance over the previous 5 years, please reference Exhibit 6.

You see almost half of those first-year returns frequently occurring in the first three months. Most of the time, being invested for the beginning of the V-bounce up means big returns.

Keep in mind that the bounce may not always look like a bounce at first—it may feel choppy. But over time, the V will become apparent when looking back. If you believe equities won’t boom off the bottom, you better have a darned good reason to expect it. Equities are resilient. That’s no myth.

Appendix

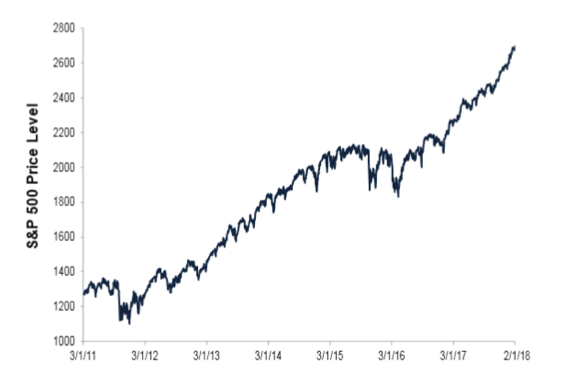

Exhibit 6: S&P 500 Price Index Level, 2011-2018

Source: FactSet, as of 24/07/2018. S&P 500 Price Index Level, from 03/01/2011 to 02/01/2018. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns.

Fisher Investments Europe Limited, trading as Fisher Investments UK, is authorised and regulated by the UK Financial Conduct Authority (FCA Number 191609) and is registered in England (Company Number 3850593). Fisher Investments Europe Limited has its registered office at: 2nd Floor, 6-10 Whitfield Street, London, W1T 2RE, United Kingdom.

Investment management services are provided by Fisher Investments UK’s parent company, Fisher Asset Management, LLC, trading as Fisher Investments, which is established in the US and regulated by the US Securities and Exchange Commission.

Investing in financial markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance neither guarantees nor reliably indicates future performance. The value of investments and the income from them will fluctuate with world financial markets and international currency exchange rates.

Follow the latest market news and updates from Fisher Investments UK:

[i] The S&P 500 Total return Index is based upon GFD calculations of total returns before 1971. These are estimates by GFD to calculate the values of the S&P Composite before 1971 and are not official values. GFD used data from the Cowles Commission and from S&P itself to calculate total returns for the S&P Composite using the S&P Composite Price Index and dividend yields through 1970, official monthly numbers from 1971 to 1987 and official daily data from 1988 on.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Global Financial Data, Inc., as of 31/12/2018, S&P 500 price returns.

Comments