Have you ever seen a headline saying equity markets are “too high”? Or that a market fall is right around the corner due to overvalued equities, or “dangerous” all-time highs? Some investors fear that equities reaching new heights means a downturn is right around the corner. Although acrophobia—the fear of heights—may have been a useful human behaviour in the past when it came to staying physically safe from falling off actual cliffs and the like, the intuition involved does not directly apply to equity markets and their heights.

Before judging the effect of “too high” equity prices, first you must use an appropriate framework. Sometimes fears of market highs come from not scaling historical market performance correctly. Take a look at Exhibit 1, which shows the US S&P 500 Total Return Index—an American stock market index—on a linear scale.

Exhibit 1: S&P 500 Total Return Index (Linear Scale)

Source: Global Financial Data as of 01/02/2019; S&P 500 Total Return Index Level from 31/12/1925 – 31/01/2019. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns.

This chart does seem to show some scary, steep heights. It makes it appear as if the last ~10 years have had unreasonable, steeply climbing returns, while most of the rest of the index’s history has only seen slowly rising prices.

However, looks can be deceiving. This linear scale shows the compounded returns over the entire time period, without accounting for the cumulative effect of long-term growth. Thought of in a different way, equity indexes don’t reset to zero overnight. The growth an index experiences in one period sticks around for the next period and can add to future growth. This means that if an index rises over time, the number that represents that index keeps growing larger. But the linear scale doesn’t account for that base-level growth over time when displaying current market movements. Although linear scales can be useful for many things, including shorter term market movements, they are not always as effective when taking a broader view of market history

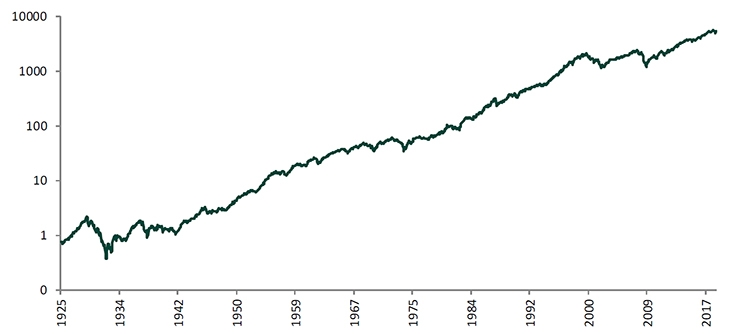

What’s a better way to look at long-term equity market returns? See Exhibit 2, which shows the exact same index returns, only plotted on a logarithmic scale.

Exhibit 2: S&P 500 Total Return Index (Logarithmic Scale)

Source: Global Financial Data as of 01/02/2019; S&P 500 Total Return Index Level from 31/12/1925-31/01/2019. Presented in US dollars. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns.

This growth looks much more reasonable, without the incredible recent steepness of the previous graph. How is this so? A logarithmic scale is based on orders of magnitude and presents equal percent changes as the same vertical moves. It takes into account cumulative growth over time and changes are displayed as percentage growth.

For example, on a linear scale, an increase from 200 to 400 looks the same as that from 2,200 to 2,400. But the increase from 200 to 400 is a massive increase—100 percent. Whereas an increase from 2,200 to 2,400 is less than a 10% increase. If an index continues to grow and compound over time, as shown in Exhibit 1, the same numerical intervals of price changes mean less from a percentage change standpoint.

On the logarithmic scale, an increase from 200 to 400 would look quite different than one from 2,200 to 2,400. The 200 to 400 increase would instead look the same as that from 2,000 to 4,000, as they are both a 100% increase. This representation of percentage differences helps us see market changes the way that we and our portfolios actually experience them. If an index experiences a gain of 100 points, but was already at 10,000 points, that is less impactful than a gain of 100 points when the index was previously at 10 points.

Once we have figured out how to scale market returns in such a way that we can observe the percent changes over time, we see that in Exhibit 2, although the market has continued to rise and reach new highs over time, it has not been in one, sudden, steep swoop. Recent index growth has not grown wildly out of control when compared to the index history. There are some times of steeper rises and declines, but they have occurred throughout the index’s history.

You can also see that the index has grown over time, frequently hitting new highs. In fact, in order for the market to rise over the long term, it has to continue to hit new highs from a mathematical perspective. Bull markets—periods of generally rising equity prices—have varying length and steepness. Just because the market has gained a certain amount in a certain time frame does not mean it will fall once it reaches a preset threshold. Past performance does not predict future returns. New highs are not predictions of impending downturns.

If specific market heights aren’t necessarily bad omens to watch out for, what can investors do? Instead of watching the index level, it may be more worthwhile to evaluate how investors are reacting to the new highs. Are headlines touting the dangers of the new highs? This investor pessimism is not necessarily a negative. In fact, it is often when investor sentiment has grown from optimism to euphoria that signals you may be at the market’s top. The time to take pause is when investors are dismissing or underappreciating fundamental negatives.

So when you hear or see news concerning the danger of equity markets’ new highs, pause and consider the following: have you scaled the markets in an appropriate fashion? Does investor sentiment seem to be overly pessimistic based solely on this “new high” news? When considering fundamentals, should you be wary of this new milestone? New equity market highs mean the market has grown. If markets continue to grow, there will continue to be new highs—and the same fears. Don’t fall prey to that fear without reason.

Get exclusive stock market knowledge in your free Markets Commentary guide and receive ongoing insights.

Fisher Investments Europe Limited, trading as Fisher Investments UK, is authorised and regulated by the UK Financial Conduct Authority (FCA Number 191609) and is registered in England (Company Number 3850593). Fisher Investments Europe Limited has its registered office at: 2nd Floor, 6-10 Whitfield Street, London, W1T 2RE, United Kingdom.

Investment management services are provided by Fisher Investments UK’s parent company, Fisher Asset Management, LLC, trading as Fisher Investments, which is established in the US and regulated by the US Securities and Exchange Commission. Investing in financial markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance neither guarantees nor reliably indicates future performance. The value of investments and the income from them will fluctuate with world financial markets and international currency exchange rates.

Comments