Whenever the US Federal Reserve (the Fed) – the central bank of the United States – appears to be raising or lowering interest rates, investors invoke a common phrase: “Don’t fight the Fed”. The premise behind this saying is an investor belief that when the Fed (or any central bank) raises interest rates, the move hurts equities. Conversely, equities benefit when a central bank lowers rates. The saying implies investors are foolish to sell equities when a central bank is cutting rates or to buy equities when rates are rising.

Understanding the relationship between central bank policy changes and equity returns is particularly important for investors today because the Fed and other central banks are poised to begin raising interest rates for the first time in years. Fisher Investments UK believes markets are far too complex to give such simple turns of phrase any true predictive power. That’s why we suggest you be wary of this proverb, since historical evidence doesn’t support the view that rate hikes spell disaster for equities.

History shows little reliable evidence

If “Don’t fight the Fed” was a reliable trading strategy, historical returns would show a strong inverse relationship between central bank rate moves and equity returns (i.e. rates go up and equities go down, and vice versa). You can test a market hypothesis or clever-sounding market saying by consulting historical returns. In the absence of such a test, investors can’t really determine if a particular strategy is effective or mere speculation.

Fortunately, testing the “Don’t fight the Fed” axiom is straightforward. For example, the Fed steadily cut US rates from 2001 to 2003; however, global equities tanked over that period. If you followed the logic of this old adage, the moment the Fed cut rates would have been a good time to buy equities – yet it wasn’t. Similarly, the Fed raised rates 17 times between 2004 and 2006, but the bull market underway at the time continued unabated.

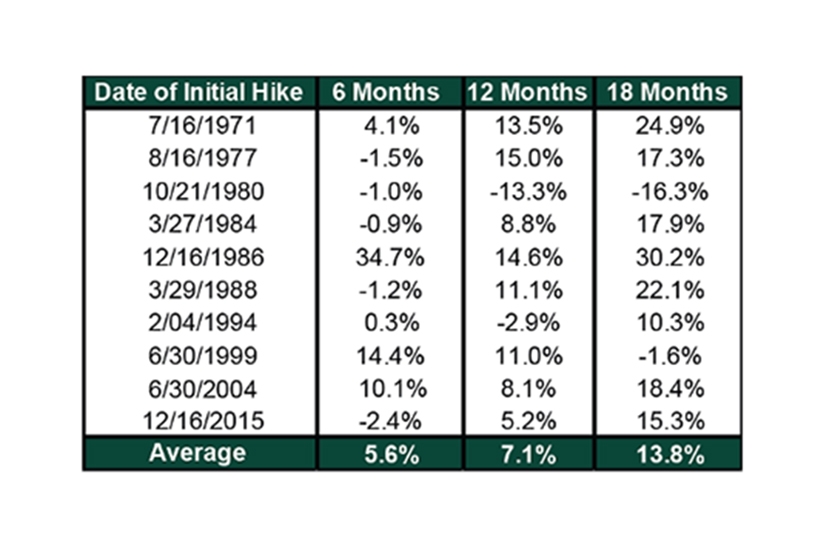

Even with a longer-term view, there’s scant evidence that “Don’t fight the Fed” is a reliable investing strategy. The exhibit below shows global equity returns in the months following initial interest rate hikes since the early 1970s. On average, equity returns are positive in most 6-, 12- and 18-month periods following an initial rate hike.

Exhibit: MSCI World Returns After US Federal Reserve Rate Hikes

Source: Fisher Investments Research; FactSet; as of 17/11/2017. Returns are in US dollars. International currency fluctuations can impact returns.

In reality, equities can rise or fall whether interest rates are on their way up or down. What’s more, the magnitude and timing of central bank rate changes matter, too. For example, whilst large rate moves over a short period might rattle markets, gradual moves – up or down 0.25%, 0.5% or even 1.0% – likely don’t have much long-term effect in either direction for equities.

Central bank decisions need context

How the interest rate decision compares with investors’ expectations can also affect how central banks’ monetary policy moves impact markets. A great example of a central bank acting in a way that defied investor expectations is the European Central Bank’s (ECB) move in the second quarter of 2011. The ECB increased short-term rates from 1% to 1.5% over just a couple of months. This unexpected move panicked investors and choked lending activity, which slowed the region’s economic activity and deepened the European recession.

Be mindful, but not myopic

Whilst “Don’t fight the Fed” isn’t a totally reliable investing mantra, ignoring central bank decisions altogether can also be a bad idea for investors. Fisher Investments UK believes it’s prudent to be mindful of monetary policy decisions, given their outsized potential impact when central banks go wildly astray.

Don’t reduce interest rate moves to a single data point. Consider relevant context that reflects the size, scale and trend of rate changes. The backdrop of economic, political and sentiment drivers that surround rate moves is also increasingly important. Central bank monetary policy decisions are important, but they are always part of a broader perspective.

Most long-term investors or retirement savers need equity-like growth to reach their investment goals. As such, they need to be invested through all market conditions. If you gamble and try to choose when you’re invested – whether by not trying to “fight” central bank policies or some other strategy – you’re often more likely to hurt your long-term results and jeopardise your financial objectives.

Interested in other topics by Fisher Investments UK? Get our ongoing insights, starting with a copy of 10 Retirement Investment Blunders to Avoid.

Follow the latest market news and updates from Fisher Investments UK:

Facebook: https://facebook.com/FisherInvestmentsUK/

Twitter: https://twitter.com/FisherInvestUK

LinkedIn: https://www.linkedin.com/company/fisher-investments-uk

Fisher Investments Europe Limited, trading as Fisher Investments UK, is authorised and regulated by the UK Financial Conduct Authority (FCA Number 191609) and is registered in England (Company Number 3850593). Fisher Investments Europe Limited has its registered office at: Level 18, One Canada Square, Canary Wharf, London, E14 5AX, United Kingdom.

Investment management services are provided by Fisher Investments UK’s parent company, Fisher Asset Management, LLC, trading as Fisher Investments, which is established in the US and regulated by the US Securities and Exchange Commission. Investing in financial markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance neither guarantees nor reliably indicates future performance. The value of investments and the income from them will fluctuate with world financial markets and international currency exchange rates.

Investing in equity markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance is no guarantee of future returns. International currency fluctuations may result in a higher or lower investment return. This document constitutes the general views of Fisher Investments UK and should not be regarded as personalised investment or tax advice or as a representation of its performance or that of its clients. No assurances are made that Fisher Investments UK will continue to hold these views, which may change at any time based on new information, analysis or reconsideration. In addition, no assurances are made regarding the accuracy of any forecast made herein. Not all past forecasts have been, nor future forecasts will be, as accurate as any contained herein.

Comments