In the world of investing, fixed interest is often associated with being a “safe” investment option. After all, the name fixed interest implies the income you receive is a “fixed” amount. This school of thought often leads investors who have long-term growth needs to forgo potentially better growth opportunities for what they consider to be safer investment options. But just how safe are fixed interest securities? The answer depends on your definition of “safe.”

Does your definition of safe mean a higher probability of low short-term volatility? If so, you could consider fixed interest a safe option. But if your definition of safe means increasing the probability of growing your retirement portfolio enough to support your income needs in retirement, fixed interest might not be your best option. If you require a certain level of growth to maintain your current lifestyle in retirement, and you have primarily invested in fixed interest throughout your career, you may not feel as safe when you discover your retirement savings might not last as long as you anticipated or is not free from volatility.

Fixed Interest Is Not Exempt From Volatility

There is no questioning that stocks can be volatile. However, volatility is not a feature exclusive to stocks. Fixed interest securities have the ability to lose value in the short term as well. Fixed interest prices move in an inverse or opposite direction to interest rates. This means when interest rates fall, fixed interest prices rise. So while coupon payment may stay the same, as interest rates change fixed interest prices fluctuate. Of course, some categories of fixed interest are more volatile than others, meaning they will have larger movements in price. In fact, with many European government fixed interest securities yielding negative interest rates, negative returns are no longer even uncommon.

Over shorter periods of time, fixed interest is typically less volatile than equities.[i] The emphasis in the previous sentence should be over shorter periods of time. Over a year or even five, fixed interest is less volatile on average. Unfortunately, because you are taking on less volatility in the short term, you can also generally expect lower returns over longer time periods. If your goal is to avoid volatility and you do not require greater long-term growth, then fixed interest securities may be an optimal choice for you.

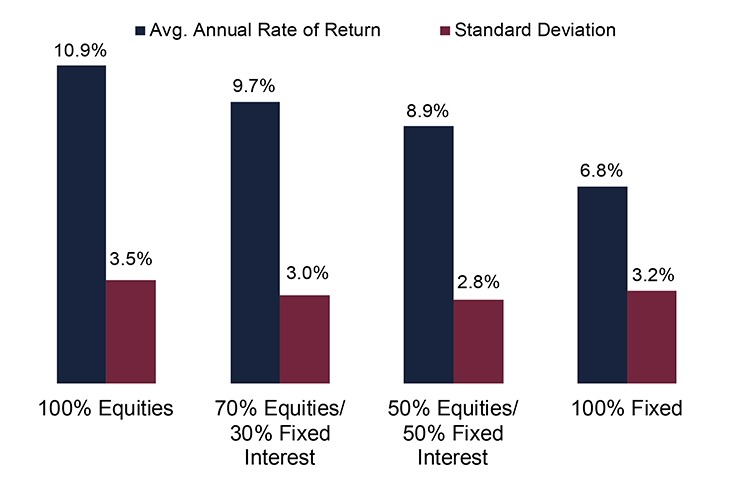

Exhibit 1 shows the average annualised return and standard deviation (a common measure of volatility) over a 5-year period for a portfolio of 100% equites, 70% equities 30% fixed interest, 50% equities 50% equities and 100% fixed interest.

Exhibit 1: 5-Year Time Horizon

Standard deviation represents the degree of fluctuations in historical returns. The risk measure is applied to 5-year annualised returns in the foregoing chart.

Source: Global Financial Data, Inc. (GFD); as of 31/12/2018. Based average returns over 5-year rolling periods based on GFD’s World Index returns from 1926-2018. GFD’s World Return Index in Great British Pounds (GBP). The World Return Index is based upon GFD calculations of total returns before 1970. These are estimates by GFD to calculate the values of the World Index before 1970 and are not official values. GFD used specified weightings to calculate total returns for the World Index through 1969 and official daily data from 1970 on. Fixed Interest return based on GFD’s Global US Dollar Total Return Government Bond Index and converted to GBP.

Not surprising to many, 100% stocks had the highest return and 100% fixed interest had the lowest standard deviation over a 5-year time period. As you see with the different asset allocations, the more fixed interest in a portfolio, the less volatility that the hypothetical portfolio incurred.

What may surprise you, however, is what happens to these numbers when you increase the time horizon to 30 years.

Exhibit 2: 20-Year Time Horizon

Standard deviation represents the degree of fluctuations in historical returns. The risk measure is applied 20-year annualised returns in the foregoing chart.

Source: Global Financial Data, Inc. (GFD); as of 31/12/2018. Based on average returns over 20-year rolling periods based on GFD’s World Index returns from 1926-2018. GFD’s World Return Index in Great British Pounds (GBP). The World Return Index is based upon GFD calculations of total returns before 1970. These are estimates by GFD to calculate the values of the World Index before 1970 and are not official values. GFD used specified weightings to calculate total returns for the World Index through 1969 and official daily data from 1970 on. Fixed Interest return based on GFD’s Global US Dollar Total Return Government Bond Index and converted to GBP.

Whilst the 100% equity portfolio still has the highest returns over that 20-year time period, it also has a similar standard deviation to other portfolios over that time. Remarkably, equities not only have comparable volatility over that time period, but they also have higher returns.

If you own equities, on a daily, monthly and even yearly basis, stocks experience heightened volatility, especially when compared to fixed interest. Dealing with that volatility can be emotionally draining, to say the least. If your financial needs will require higher investment returns, heightened short-term volatility can be thought of as “the price you will pay for those returns.” This is what we often refer to as the risk-return tradeoff for participating in equities’ historically high returns. So whilst it may be surprising to hear, over the long term, equities have been less volatile than fixed interest!

Don’t Forget About Inflation’s Impact

It’s surprising to see how many investors fail to account for the impact of inflation. If at some point during your investment time horizon (the amount of time you need your retirement savings to last) there is a period of high inflation, you could be impacted two ways.

First, when inflation rises, so do long-term interest rates. Since fixed-interest yields and prices have an inverse relationship, the value of your long-term fixed interest securities will fall accordingly.

Second, when your fixed income starts paying you back, the money you are being paid out is less valuable—due to the impact of inflation.

In G20 nations, many central banks target a 2-3% inflation rate, meaning if you are not seeing investment returns eclipsing 3%, your money could be losing value on an annual basis. In order to combat inflation’s impact, you may require growth-oriented investments—such as equities—in your retirement portfolio. Failing to account for the insidious effect of inflation can mean running out of money faster than you anticipated—meaning a retirement portfolio consisting of 100% fixed interest may not be as safe as you thought.

Interested in other topics by Fisher Investments UK? Download your free copy of Markets Commentary and receive ongoing insights.

Fisher Investments Europe Limited, trading as Fisher Investments UK, is authorised and regulated by the UK Financial Conduct Authority (FCA Number 191609) and is registered in England (Company Number 3850593). Fisher Investments Europe Limited has its registered office at: 2nd Floor, 6-10 Whitfield Street, London, W1T 2RE, United Kingdom.

Investment management services are provided by Fisher Investments UK’s parent company, Fisher Asset Management, LLC, trading as Fisher Investments, which is established in the US and regulated by the US Securities and Exchange Commission. Investing in financial markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance neither guarantees nor reliably indicates future performance. The value of investments and the income from them will fluctuate with world financial markets and international currency exchange rates.

[i] Source: Global Financial Data, as of 09/01/2019. Based on standard deviation over 5- and 30-year rolling periods from 31/12/1925 – 31/12/2018. Equity return based on the S&P 500 Total Return Index. Fixed income return based on Global Financial Data’s USA 10-Year Government Bond Index. Currency fluctuations may result in higher or lower investment returns.

Comments