Today’s budget forecasts a £20bn reduction in the tax receipts by 2021-22. That’s the cost of the productivity downgrade:

The Treasury got a £9bn windfall this year from a lower borrowing forecast. That’s the same as the £9bn peak fiscal loosening in 2019-20:

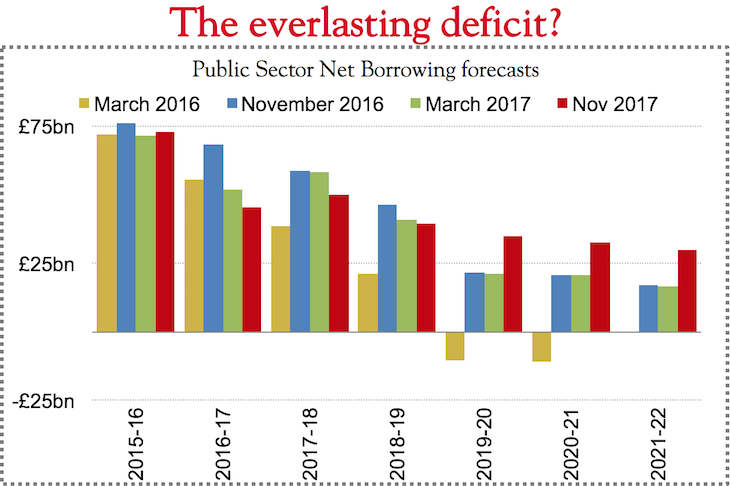

The £14bn higher borrowing by the end of the period is roughly the same as £13bn higher borrowing in 2019-20. But in 2019-20, most of that is £9bn of giveaways (which fall away in the final two years). By the end, the fiscal deterioration is, basically, lower tax receipts as a result of slower growth:

So we have fiscal loosening and higher borrowing. Still, the deficit is still forecast to be low as a percentage of GDP – below two per cent and falling towards one per cent. Okay for now, especially while Brexit uncertainty remains:

But we need to stay focused on getting absolute levels of government debt down (as a percentage of GDP) before the next crisis hits. Even with deficits below two per cent of GDP, look how slowly debt is forecast to fall as a percentage of GDP:

We’ve made a lot of progress reducing the structural deficit. Are we now content to let it drift down slowly – or level off – at these levels?

Rupert Harrison is former chief of staff to George Osborne and a portfolio manager at Blackrock

Rupert Harrison is former chief of staff to George Osborne and a portfolio manager at Blackrock

Comments