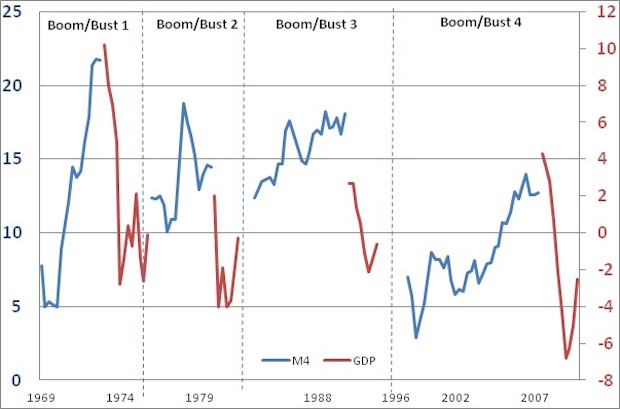

Here is a graph that shows the four economic downturns Britain has been through (red lines) over the past forty years.

What I find strking is that each downturn was preceded by the same thing: a surge in the growth of money (blue line). In other words, the bust followed an unsustainable credit-induced boom.

The motives and justification behind monetary policy leading up to each boom/bust might have been different. In the early 1970s, monetary policy was shaped by Competition and Credit Control (CCC) reforms. In the late 1980s, those who decided monetary policy wanted to shadow the Deutschemark, then join the Exchange Rate Mechanism (ERM). After that unhappy experience, monetary policy was made in order to target inflation.

No matter what those in charge thought they were doing – CCC, ERM or inflation targeting – as the blue lines show, they nonetheless presided over an unsustainable growth in the money supply. Which was followed by a sharp downturn.

In a paper on monetary policy published in the House of Commons tomorrow, I argue that we are in danger of repeating the same mistakes again. Yet another growth in money and credit – which will be followed by yet another falling red line on the graph.

Many of the warning signs of yet another credit-induced boom are already there; increasing reliance on consumer spending, surging house prices, falling savings ratio and a deteriorating current account balance.

What ought we to do about it?

First, we need a tighter monetary policy, with higher interest rates. But we also need some more far reaching change in the way we run the economy, too.

One of the reasons, I suggest in my paper, why successive administrations have failed to prevent these credit bubbles is not merely down to misjudgement. Part of the problem is that banks are able to conjure credit out of thin air.

Preventing endless boom/busts requires real banking reform. In my paper I suggest how we might prevent runaway credit bubbles forming – but using the free market, rather than the flawed judgement of central bankers or regulators.

Although the Bank of England might not have met its inflation target for many months, it has delivered lower, and more stable, inflation. In the twenty years since inflation targeting began, inflation has average 2.1 per cent – compared to 12 per cent in the 1970s and 6 per cent in the 1980s.

But low and stable inflation on one side of the equation has seen bank busts and credit crunches on the other. As long as banks lending is simply a function of their appetite to lend, combined with the appetite of borrowers to borrow – and restrained only by regulators – this fundamental instability will remain. A banks ability to lend must also be a function of its deposits. My paper proposes a simply way of achieving this.

If we are to avoid boom/bust 5, we need to change the way we manage the money. I hope my paper and its suggestions help. I suspect at some point in the future we might need new ideas on monetary reform.

Douglas Carswell’s paper After Osbrown is published by Politeia tomorrow.

Comments